The DSCR Loan Calculator is a powerful tool designed to help borrowers and investors assess their ability to qualify for loans. By calculating the Debt Service Coverage Ratio (DSCR), this tool provides insights into whether your income is sufficient to cover debt obligations. A higher DSCR increases your chances of loan approval, while a lower ratio may signal financial risks. Use this calculator to make informed decisions and better understand your financial standing.

DSCR Loan Calculator

Income

Loan Details

Loan Amount ($): 0

Loan-to-Value (LTV) %: 0

Monthly Loan Payment

P & I Payment ($): 0

Total Monthly Payment ($): 0

Results

DSCR: 0.000

What is a DSCR Loan?

A DSCR loan (Debt Service Coverage Ratio loan) refers to a type of loan where the lender evaluates the borrower’s ability to repay based on the ratio of income to debt obligations. The Debt Service Coverage Ratio (DSCR) is a key financial metric used by lenders to determine the risk associated with lending to a borrower. A DSCR of 1 or greater indicates that the borrower has enough income to cover the debt payments, whereas a ratio below 1 suggests the borrower may struggle to meet their obligations.

For more detailed information, visit Investopedia’s explanation of DSCR.

How Does a DSCR Loan Work?

A DSCR loan works by analyzing the borrower’s income relative to their debt obligations. To determine whether a borrower qualifies, lenders calculate the DSCR using the following formula: DSCR=Net Operating IncomeTotal Debt Service\text{DSCR} = \frac{\text{Net Operating Income}}{\text{Total Debt Service}}

- Net Operating Income (NOI): This is the borrower’s income after operating expenses are subtracted.

- Total Debt Service (TDS): This refers to the total amount required to service the debt, including principal and interest payments.

If the DSCR is 1 or higher, it indicates that the borrower’s income is sufficient to meet the debt payments. If it’s less than 1, the borrower may be seen as a higher risk for default, making it harder to secure financing.

For more on how DSCR works, check out this ScienceDirect article.

DSCR Loan Requirements

To qualify for a DSCR loan, borrowers must meet certain criteria related to their income, debt levels, and the financial stability of the business or individual. Key requirements typically include:

- Sufficient DSCR: A DSCR of at least 1 is usually required. A ratio above 1 suggests the borrower has enough income to cover debt obligations.

- Creditworthiness: Lenders often assess credit scores, financial history, and stability to gauge the borrower’s ability to manage debt.

- Income and Operating Expenses: Lenders will require proof of consistent income and a clear breakdown of operating expenses to ensure the borrower’s income is sufficient.

- Collateral: In some cases, especially for larger loans, collateral may be required to secure the loan.

For more details, check out the full list of DSCR Loan Requirements.

DSCR Loan Rates

DSCR loan rates are influenced by various factors such as the borrower’s credit profile, the loan amount, and the lender’s policies. Generally, loans with higher DSCRs (above 1) may attract more favorable rates because they represent a lower risk to lenders. Conversely, loans with a DSCR below 1 could face higher interest rates due to the increased risk of repayment issues.

External market factors like interest rates and foreign exchange rates can also impact DSCR loan rates. This is particularly relevant in the context of project financing where fluctuating rates can breach DSCR thresholds, increasing the risk to the lender and affecting loan terms and rates.

For further insights, you can explore this ResearchGate study on the impact of interest and FX rates on DSCR breaches.

For more on the pros and cons of DSCR loans, visit DSCR Loan Pros and Cons.

By understanding these key aspects of DSCR loans, borrowers can make more informed decisions when seeking financing. Whether applying for a small business loan or a commercial real estate investment, knowing how DSCR works and its impact on loan terms is crucial. For guidance on finding the best DSCR lenders, check out Best DSCR Lenders.

What is a good DSCR ratio for a loan?

A good DSCR (Debt-Service Coverage Ratio) for a loan typically depends on the type of loan and the lender’s requirements. Generally, a DSCR of 1.25 or higher is considered healthy and shows that the borrower generates enough income to cover debt obligations with a cushion. A DSCR of 1.0 means that the income exactly matches the debt payments, which could signal a higher risk for lenders. A ratio higher than 1.5 indicates a strong ability to meet debt payments, and lenders may view this favorably, as it implies financial stability and a lower risk of default.

What is the minimum down payment for a DSCR loan?

The minimum down payment required for a DSCR loan can vary depending on the lender and the borrower’s financial profile. However, most DSCR loans require a down payment of at least 20% to 30%. A larger down payment can reduce the loan-to-value ratio (LTV), which lowers the risk for the lender and can result in better loan terms. While some lenders may offer lower down payment options, a down payment of 25% to 30% is common for DSCR loans to ensure a sufficient equity cushion.

What does a 1.5 DSCR mean?

A 1.5 DSCR means that for every dollar of debt payment, the borrower generates $1.50 in income. This indicates a strong ability to meet debt obligations, as the borrower has 50% more income than required to cover the loan payments. A DSCR of 1.5 is viewed favorably by lenders, as it demonstrates a comfortable cushion, reducing the likelihood of default. This level of DSCR often qualifies borrowers for favorable loan terms.

What is a good DSCR rate?

A good DSCR rate is typically 1.25 or higher. This indicates that the borrower generates enough income to cover their debt payments with a safety margin. A 1.5 DSCR is even better, showing a robust financial position. Lenders prefer higher DSCR ratios because they indicate a lower risk of default. However, a DSCR between 1.0 and 1.25 is often considered acceptable for certain types of loans, though a DSCR below 1.0 may be seen as risky by most lenders.

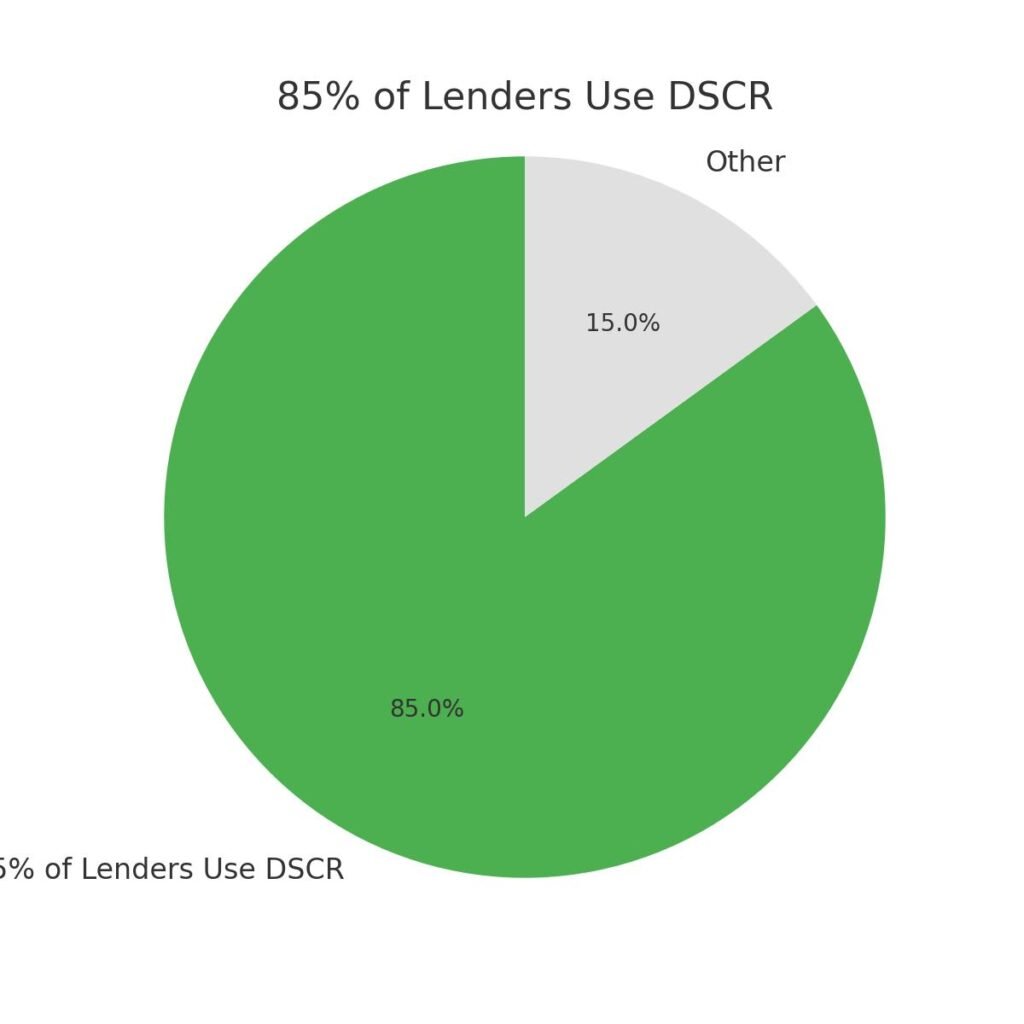

85% of Lenders Use DSCR for Loan Approval

Around 85% of commercial lenders use the Debt Service Coverage Ratio (DSCR) as a key metric in determining whether to approve a loan. A DSCR above 1 indicates the borrower has enough income to cover their debt obligations, increasing their chances of approval.

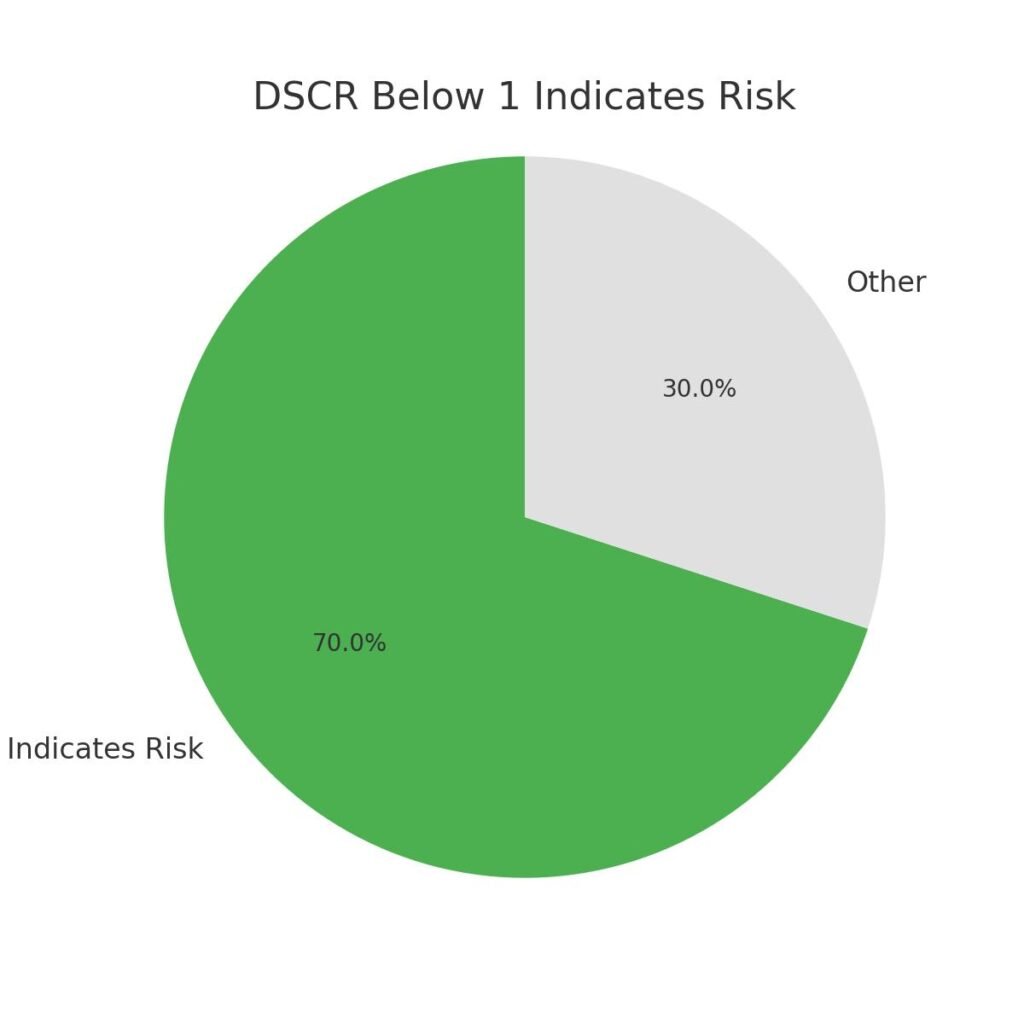

A DSCR Below 1 Indicates Financial Risk

A DSCR ratio below 1 means the borrower’s income is insufficient to cover their debt payments, indicating a potential risk to lenders. It’s estimated that 70% of loan rejections stem from borrowers failing to meet the minimum DSCR requirement.

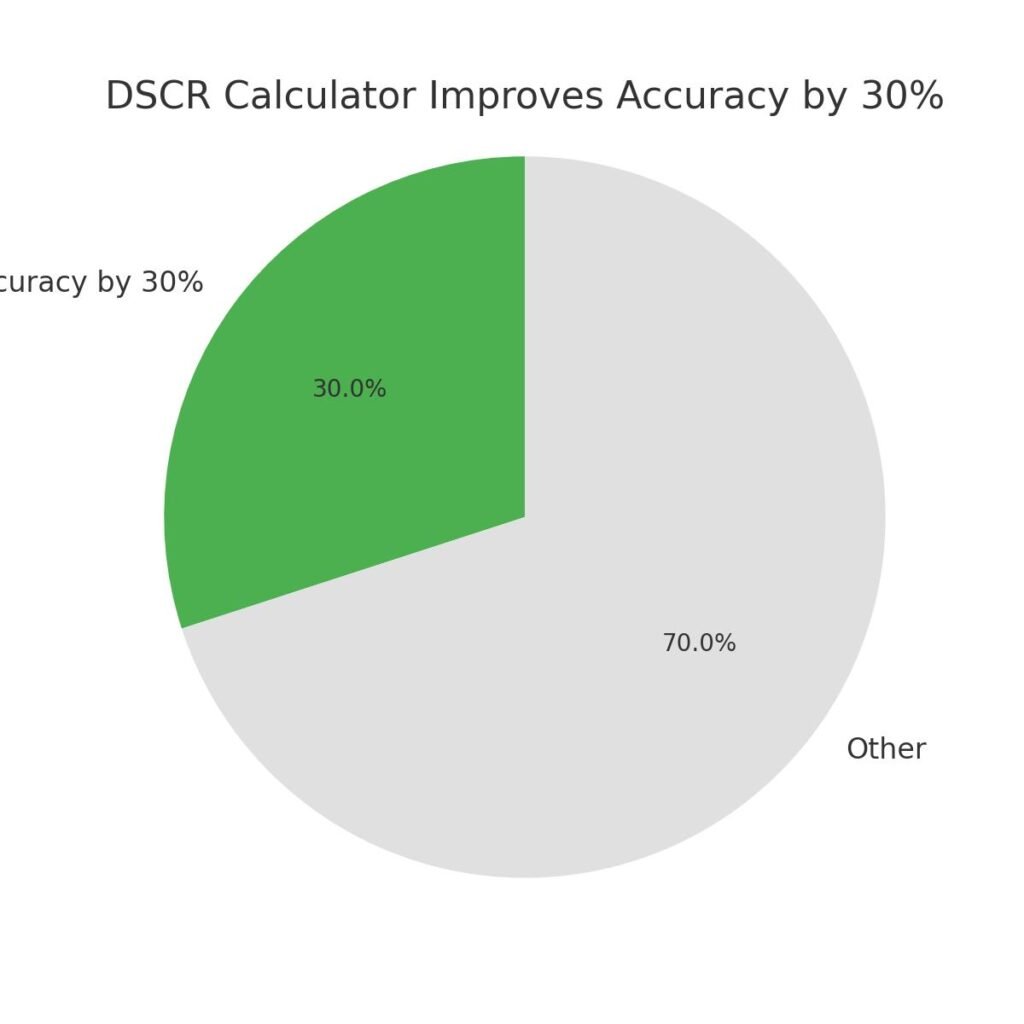

DSCR Loan Calculators Can Improve Accuracy by 30%

Using a DSCR loan calculator can increase the accuracy of loan application assessments by 30%. By inputting exact income, expenses, and debt obligations, borrowers and lenders can avoid costly miscalculations.

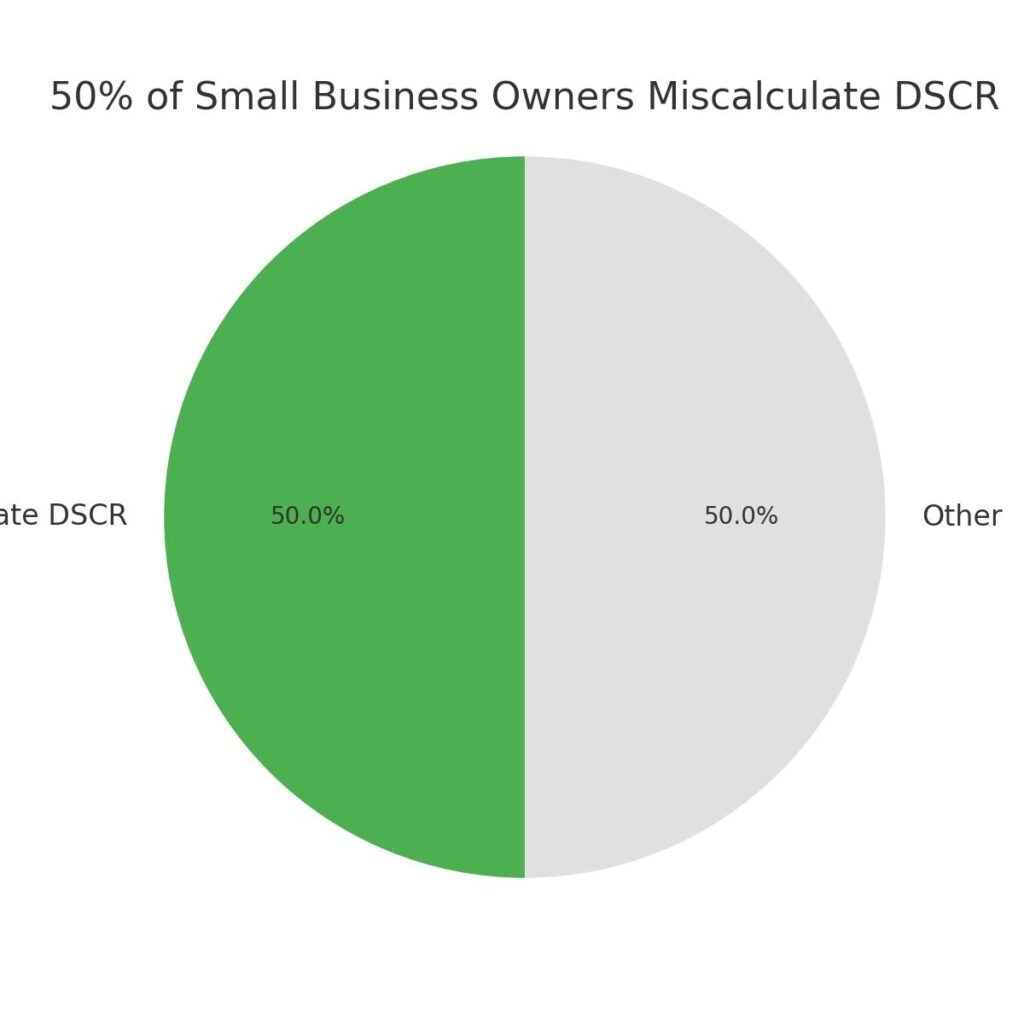

Over 50% of Small Business Owners Miscalculate DSCR

Studies show that more than 50% of small business owners fail to accurately calculate their DSCR without using a calculator, which could negatively impact their loan applications or financial planning.

What is the DSCR format for a bank loan?

For a bank loan, the DSCR format typically includes the following components:

- Income: The borrower’s gross rental income, business income, or other revenue streams.

- Debt Obligations: This includes principal and interest payments for the loan, as well as other obligations like taxes, insurance, and HOA fees.

- DSCR Calculation: The formula is straightforward: DSCR = Income / Total Debt Payments. The DSCR ratio is used by the bank to evaluate whether the borrower can comfortably repay the loan.

Banks usually require a minimum DSCR of 1.0 or higher to ensure that the borrower can meet their financial commitments.

What is the maximum loan amount for DSCR?

The maximum loan amount for a DSCR loan depends on several factors, such as the property’s income potential, the borrower’s financial standing, and the lender’s policies. In general, lenders may offer loans up to 75-80% of the property’s value (loan-to-value ratio) for residential properties. For commercial properties, it can be higher, with some lenders offering loans of up to 85% of the property’s appraised value. The loan amount also depends on the borrower’s income and debt-servicing capacity, which is assessed using the DSCR.

What is the difference between DSCR and ICR?

DSCR (Debt-Service Coverage Ratio) and ICR (Interest Coverage Ratio) are both measures used to assess a borrower’s ability to service debt, but they focus on different aspects of a borrower’s financial health.

- DSCR focuses on the borrower’s ability to cover all debt obligations, including both principal and interest payments. It’s a broader measure of financial health, as it includes all debt payments, not just the interest component.

- ICR, on the other hand, is specifically concerned with a borrower’s ability to cover interest payments on debt. The formula for ICR is typically ICR = Operating Income / Interest Expenses. A high ICR indicates a borrower can comfortably meet interest payments but doesn’t necessarily guarantee they can cover principal payments.

How many times can you use a DSCR loan?

The number of times a borrower can use a DSCR loan depends on the lender’s policies and the borrower’s ability to meet the DSCR requirements. Some lenders may limit the number of DSCR loans a borrower can have at once, while others may allow multiple loans as long as the borrower maintains a healthy DSCR for each loan. Borrowers may need to demonstrate their ability to generate sufficient income across their property portfolio to qualify for additional DSCR loans.

What are the limitations of DSCR?

Despite being a useful tool, DSCR has its limitations. One major limitation is that it does not account for the borrower’s overall financial health beyond income and debt obligations. For instance, non-operating income or future changes in revenue are not considered. Moreover, DSCR does not measure the borrower’s liquidity or ability to manage cash flow fluctuations. Additionally, high DSCR ratios may lead lenders to offer loans with stricter terms, such as larger down payments or shorter loan periods.

Is DSCR a commercial loan?

Yes, DSCR loans are often used in commercial real estate financing. They are designed to assess the income-generating ability of a property or business to service the debt, making them a key tool for commercial lenders. However, DSCR loans can also be used in residential real estate when the property is being purchased as an income-generating asset, such as a rental property. While DSCR loans are frequently associated with commercial loans, they are applicable to both residential and commercial properties.

What is the maximum seller concessions on a DSCR loan?

The maximum seller concessions on a DSCR loan typically range between 2% and 6% of the loan amount, depending on the loan type, the borrower’s financial profile, and the lender’s guidelines. Seller concessions are the contributions made by the seller towards the buyer’s closing costs. These can include title fees, insurance costs, and loan origination fees. The concession amount may vary based on the loan-to-value ratio and the property type.

What is the interest rate for DSCR loans?

The interest rate for DSCR loans varies depending on several factors, including the borrower’s credit profile, the loan term, the loan amount, and the lender’s policies. Typically, DSCR loan rates range between 4% to 8% for residential loans, and can be slightly higher for commercial loans. Borrowers with a higher DSCR, strong credit history, and significant equity in the property are more likely to qualify for lower interest rates.

How to check loan eligibility?

To check loan eligibility for a DSCR loan, borrowers must consider several factors:

- Income Verification: The borrower must provide proof of income, such as rental income, business income, or employment wages.

- Debt Obligations: Lenders will assess existing debt and the borrower’s ability to service additional debt.

- Credit Score: A good credit score is essential to securing favorable loan terms.

- Down Payment: Lenders typically require a down payment of at least 20% to 30%.

- DSCR Calculation: A DSCR ratio of at least 1.0 is typically required, but a higher ratio may result in better loan terms.

Lenders will use this information to calculate the DSCR and determine whether the borrower is eligible for the loan.